The U.S. Health Care System: An International Perspective

2016 Fact Sheet

The U.S. health care system is unique among advanced industrialized countries. The U.S. does not have a uniform health system, has no universal health care coverage, and only recently enacted legislation mandating healthcare coverage for almost everyone. Rather than operating a national health service, a single-payer national health insurance system, or a multi-payer universal health insurance fund, the U.S. health care system can best be described as a hybrid system. In 2014, 48 percent of U.S. health care spending came from private funds, with 28 percent coming from households and 20 percent coming from private businesses. The federal government accounted for 28 percent of spending while state and local governments accounted for 17 percent.[1] Most health care, even if publicly financed, is delivered privately.

In 2014, 283.2 million people in the U.S., 89.6 percent of the U.S. population had some type of health insurance, with 66 percent of workers covered by a private health insurance plan. Among the insured, 115.4 million people, 36.5 percent of the population, received coverage through the U.S. government in 2014 through Medicare (50.5 million), Medicaid (61.65 million), and/or Veterans Administration or other military care (14.14 million) (people may be covered by more than one government plan). In 2014, nearly 32.9 million people in the U.S. had no health insurance.[2]

This fact sheet will compare the U.S. health care system to other advanced industrialized nations, with a focus on the problems of high health care costs and disparities in insurance coverage in the U.S. It will then outline some common methods used in other countries to lower health care costs, examine the German health care system as a model for non-centralized universal care, and put the quality of U.S. health care in an international context.

In Comparison to Other OECD Countries

The Organization for Economic Co-operation and Development (OECD) is an international forum committed to global development that brings together 34 member countries to compare and discuss government policy in order to “promote policies that will improve the economic and social well-being of people around the world.”[3] The OECD countries are generally advanced or emerging economies. Of the member states, the U.S. and Mexican governments play the smallest role in overall financing of health care.[4] However, public (i.e. government) spending on health care per capita in the U.S. is greater than all other OECD countries, except Norway and the Netherlands.[5]

This seeming anomaly is attributable, in part, to the high cost of health care in the U.S. Indeed, the U.S. spends considerably more on health care than any other OECD country.

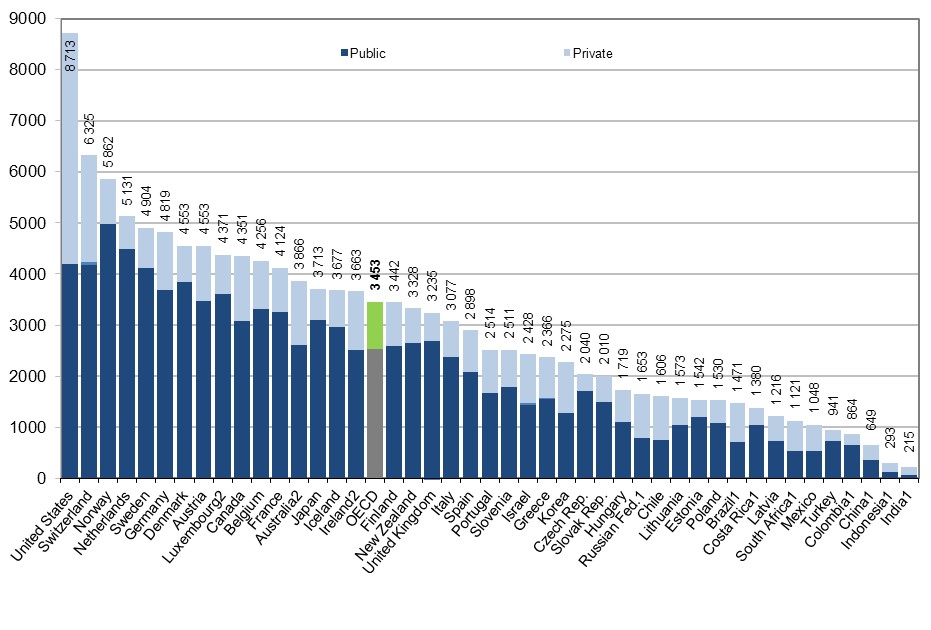

The OECD found that in 2013, the U.S. spent $8,713 per person or 16.4 percent of its GDP on health care—far higher than the OECD average of 8.9 percent per person.[6] Following the U.S. were the Netherlands, which allocated 11.1 percent of its GDP, then Switzerland also at 11.1 percent, and Sweden, which allocated 11 percent of its GDP to health care in 2013. In North America, Canada and Mexico spent respectively 10.2 percent and 6.2 percent of their GDP on health care.

On a per capita basis, the U.S. spends more than double the $3,453 average of all OECD countries (see chart[7] below).[8]

Health Expenditure per capita, 2013 (or nearest year)

Drivers of Health Care Spending in the U.S.

Prohibitively high cost is the primary reason Americans give for problems accessing health care. Americans with below-average incomes are much more likely than their counterparts in other countries to report not: visiting a physician when sick; getting a recommended test, treatment, or follow-up care; filling a prescription; and seeing a dentist.[9] Fifty-nine percent of physicians in the U.S. acknowledge their patients have difficulty paying for care.[10] In 2013, 31 percent of uninsured adults reported not getting or delaying medical care because of cost, compared to five percent of privately insured adults and 27 percent of those on public insurance, including Medicaid/CHIP and Medicare.[11]

While there is no agreement as to the single cause of rising U.S. health care costs, experts have identified three contributing factors. The first is the cost of new technologies and prescription drugs. Some analysts have argued “that the availability of more expensive, state-of-the-art medical technologies and drugs fuels health care spending for development costs and because they generate demand for more intense, costly services even if they are not necessarily cost-effective.”[12]In 2013, the U.S. spent $1,026 per capita on pharmaceuticals and other non-durable medical care, more than double the OECD average of $515.[13]

Another explanation for increased costs is the rise of chronic diseases, including obesity. Nationally, health care costs for chronic diseases contribute huge proportions to health care costs, particularly during end of life care. “Patients with chronic illness in their last two years of life account for about 32% of total Medicare spending, much of it going toward physician and hospital fees associated with repeated hospitalizations.”[14] The National Academy of Sciences found that among other high-income nations the U.S. has a higher rate of chronic illness and a lower overall life expectancy. Their findings suggest that this holds true even when controlling for socio-economic disparity.[15] Experts are focusing more on preventative care in an effort to improve health and reduce the financial burdens associated with chronic disease.[16] One provision of the Patient Protection and Affordable Care Act, commonly referred to as simply the Affordable Care Act (ACA), implemented in 2013, provides additional Medicaid funding for states providing low cost access to preventative care.[17]

Finally, high administrative costs are a contributing factor to the inflated costs of U.S. health care. The U.S. leads all other industrialized countries in the share of national health care expenditures devoted to insurance administration. It is difficult to determine the exact differences between public and private administrative costs, in part because the definition of “administrative” varies widely. Further, the government outsources some of its administrative needs to private firms.[18] What is clear is that larger firms spend a smaller percentage of their total expenditures on administration, and nationwide estimates suggest that as much as half of the $361 billion spent annually on administrative costs is wasteful.[19] In January 2013, a national pilot program implemented under the ACA began. The aim is to improve administrative efficiency by allowing doctors and hospitals to bundle billing for an episode of care rather than the current ad hoc method.[20]

Health Insurance in the U.S.: Uneven Coverage

While the majority of U.S. citizens have health insurance, premiums are rising and the quality of the insurance policies is falling. Average annual premiums for family coverage increased 11 percent between 1999 and 2005, but have since leveled off to increase five percent per year between 2005 and 2015.[21] Deductibles are rising even faster. Between 2010 and 2015, single coverage deductibles have risen 67 percent.[22] These figures outpace both inflation and workers’ earnings.

The lack of health insurance coverage has a profound impact on the U.S. economy. The Center for American Progress estimated in 2009 that the lack of health insurance in the U.S. cost society between $124 billion and $248 billion per year. While the low end of the estimate represents just the cost of the shorter lifespans of those without insurance, the high end represents both the cost of shortened lifespans and the loss of productivity due to the reduced health of the uninsured.[23]

Health insurance coverage is uneven and often minorities and the poor are underserved. Forty million workers, nearly two out of every five, do not have access to paid sick leave. Experts suggest that the economic pressure to go to work even when sick can prolong pandemics, reduce productivity, and drive up health care costs.[24]

There were 32 million uninsured Americans in 2014, nine million fewer than the year prior. Experts attribute this sharp decline in the uninsured to the full implementation of the ACA in 2014.[25] Of American adults who had health insurance in 2014, 73 percent had one or more full-time workers in the family and 12 percent had one or more part-time workers in the family.[26] Just 49 percent of American adults reported getting health insurance from an employer in 2014.[27]

Coverage by employer-provided insurance varies considerably by wage level. Firms with higher proportions of low-wage workers are less likely to provide access to health insurance than those with low-proportions of low-wage workers.[28]

In 2014, 11.2 percent of full-time workers were without health insurance. However, the percentage of part-time workers without insurance was 17.7 percent, a significant decrease from 24 percent in 2013, thanks in part to the Affordable Care Act. The uninsured rate among those who had not worked at least one week also decreased from 22.2 percent in 2013 to 17.3 percent in 2014.[29]

Smaller firms are significantly less likely to provide health benefits to full or part-time workers. Among all small firms (3-199 workers) in 2015, only 56 percent offered health coverage, compared to 98 percent of large firms.[30]

After the Affordable Care Act allowed for many young adults (19-25) to remain on their parents’ health plans, there was a statistically significant increase in the percentage of insured young people from 68.3 percent in 2009[31] to 82.9 percent in 2014.[32] Over the same period, the percentage of young people aged 26-34 with insurance increased from 70.9 percent to 81.8 percent.[33]

Minorities and children are disproportionately uninsured. In 2014, 7.6 percent of non-Hispanic Whites were uninsured, 11.8 percent of Blacks were uninsured, 9.3 percent of Asians, and 19.9 percent of people of Hispanic origin were uninsured.[34] The Kaiser Family Foundation has found that about 80 percent of the uninsured are U.S. citizens.[35] Among children, six percent were uninsured in 2014.[36] These children are 10 times more likely than insured children to have unmet medical needs and are five times as likely as an insured child to go more than two years without seeing a doctor.[37]

Women in the individual market often faced higher premiums than men for the same coverage. Beginning in 2014, the Affordable Care Act banned this practice, as well as denying coverage for pre-existing conditions.[38]

In 2014, 19.3 percent of the population living below 100 percent of the poverty line ($23,550 a year for a family of four) was uninsured.[39] According to the Kaiser Family Foundation, 90 percent of the uninsured have family incomes within 400 percent of the federal poverty level. This makes them eligible for either subsidized coverage through tax credits or expanded Medicaid eligibility under the Affordable Care Act’s state health exchanges. [40]

Rising Healthcare Premiums

Health insurance premiums in the U.S. are rising fast. From 2005 to 2015, average annual health insurance premiums for family coverage increased 61 percent, while worker contributions to those plans increased 83 percent in the same period. This rate of increase outpaces both inflation and increases in workers’ wages.[41]

In 2005, the average annual premiums for employer-sponsored health insurance were $2,713 for single coverage and $8,167 for family coverage. In 2015, premiums more than doubled to $6,251 for employer-sponsored single coverage and $17,545 for employer-sponsored family coverage.[42]

A growing number of workers face a deductible of $1,000 or more for individual plans. In 2015, 46 percent (compared to 38 percent in 2013 and 22 percent in 2009) of workers were enrolled in a plan with an annual deductible of $1,000 or more. Employees at small firms are more likely than those at large firms to have a deductible greater than $1,000.[43]

The Union Difference: Union workers are more likely than their nonunion counterparts to be covered by health insurance and paid sick leave. In March 2015, 95 percent of union members in the civilian workforce had access to medical care benefits, compared with only 68 percent of nonunion members. In 2015, 85 percent of union members in the civilian workforce had access to paid sick leave compared to 62 percent of nonunion workers.[44] At the median, private-sector unionized workers pay 38 percent less for family coverage than private-sector nonunionized workers, according to a 2009 study.[45]

Across states, there are significant disparities in both the availability and the cost of health care coverage.

In 2012, Medicare reimbursements per enrollee varied from $6,724 in Anchorage, Alaska to $13,596 in Miami, Florida.[46] Annual premiums are similarly disparate. In 2015, the average family premium in the South was $16,785 while the same coverage averaged $18,096 in the Northeast.[47]

Firms in the South were less likely to provide coverage for an employee’s domestic partner than other regions. In the South, 41 percent of firms reported providing benefits for same-sex partners (compared to 51 percent in the Northeast) and 20 percent reported offering benefits to opposite-sex domestic partners (compared to 46 percent in the Northeast).[48]

High Costs Drive Americans into Bankruptcy

Universal coverage, in countries like the United Kingdom, Switzerland, Japan, and Germany makes the number of bankruptcies related to medical expenses negligible.[49] Conversely, a 2014 survey of bankruptcies filed between 2005 and 2013 found that medical bills are the single largest cause of consumer bankruptcy, with between 18 percent and 25 percent of cases directly prompted by medical debt.[50] Another survey found that in 2013, 56 million Americans under the age of 65 had trouble paying medical bills.[51] Another 10 million will face medical bills they are unable to pay despite having year-round insurance.[52]

It has been suggested, based on the experience of Massachusetts, where medical-related bankruptcies declined sharply after the state enacted its health reform law in 2006, that the ACA may help reduce such bankruptcies in the future.[53]

The Affordable Care Act: Successes and Remaining Challenges

In March, 2010, President Obama signed the ACA into law that made hundreds of significant changes to the U.S. healthcare system between 2011 and 2014. Provisions included in the ACA are intended to expand access to healthcare coverage, increase consumer protections, emphasizes prevention and wellness, and promote evidence- based treatment and administrative efficiency in an attempt to curb rising healthcare costs.

Beginning in January 2014, almost all Americans are required to have some form of health insurance from either their employer, an individual plan, or through a public program such as Medicaid or Medicare. Since the so-called “individual mandate” took effect, the total number of nonelderly uninsured adults dropped from 41 million in 2013 to 32.3 million in 2014.[54] The largest coverage gains were concentrated among low-income people, people of color, and young adults, all of whom had high uninsured rates prior to 2014.[55]

A major provision of the ACA was the creation of health insurance marketplace exchanges where individuals not already covered by an employer-provided plan or a program such as Medicaid or Medicare can shop for health insurance. Individuals with incomes between 100 percent and 400 percent of the federal poverty line would be eligible for advanceable premium tax credits to subsidize the cost of insurance. States have the option to create and administer their own exchanges or allow the federal government to do so. Currently, only 14 states operate their own exchanges.[56]

Designed to promote competition among providers and deliver choice transparency to consumers, the state-based exchanges appear to be doing just that. A recent analysis by the Commonwealth Fund found that the number of insurers offering health insurance coverage through the marketplaces increased from 2014 to 2015.[57] Additionally, there was generally no reported increase in average premiums for marketplace plans over that period. The analysis found only a modest increase in average premiums for the lowest cost plans from 2015 to 2016.[58]

The ACA also included a major expansion of the Medicaid program, although the Supreme Court ruled in 2012 that this expansion is a state option. As of November 2015, 30 states have chosen to expand Medicaid. As of 2014, adults with incomes at or below 138 percent of the federal poverty line are now eligible for Medicaid in the states that have adopted the expansion.[59]

Despite improvements to the U.S healthcare system under the ACA, a number of challenges remain. In 2014, 10.4 percent of Americans were still uninsured[60], and those with insurance still face high deductibles and premium costs. Furthermore, in the 20 states that had not expanded Medicaid, an estimated three million poor adults fall into the “coverage gap” where their incomes are above current Medicaid eligibility limits but below the lower limit of premium credits on the healthcare exchanges. The bulk of people in the coverage gap are concentrated in the South, with Texas (766,000 people), Florida (567,000), Georgia (305,000) and North Carolina (244,000) having among the highest number of uninsured.[61]

The ACA included a number of other provisions to improve healthcare access and affordability. The law banned lifetime monetary caps on insurance coverage for all new plans and prohibited plans from excluding children and most adults with preexisting conditions.[62] Insurance plans are also prohibited from cancelling coverage except in the case of fraud, and are required to rebate customers if they spend less than 85 percent (80 percent for individual and small group plans) of premiums on medical services. Additionally, the ACA established the Prevention and Public Health Fund to allocate $7 billion towards preventative care such as disease screenings, immunizations, and pre-natal care for pregnant women and between 2010 and 2015. Furthermore, $11 billion in funding for community health centers and $1.5 billion in additional funding for the National Health Service Corps was included in the law.[63]

A number of cost control provisions were included in the ACA in an attempt to curb rising medical costs. Among them is the Independent Payment Advisory Board, which will provide recommendations to Congress and the President for controlling Medicare costs if the costs exceed a target growth rate. The administrative process for billing, transferring funds, and determining eligibility is being simplified by allowing doctors to bundle billing for an episode of care rather than the current ad hoc method. Additionally, changes were made to the Medicare Advantage program that would provide bonuses to high rated plans, incentivizing these privately-operated plans to improve quality and efficiency. Furthermore, hospitals with high readmission rates will see a reduction in Medicare payments while a new Innovation Center within the Centers for Medicare and Medicaid Services was created to test new program expenditure reduction methods.[64]

Common Methods to Lower Health Care Costs

By taking an international perspective and looking to other advanced industrialized countries with nearly full coverage, much can be learned. While methods range widely, other OECD countries generally have more effective and equitable health care systems that control health care costs and protect vulnerable segments of the population from falling through the cracks. Among the OECD countries and other advanced industrialized countries, there are three main types of health insurance programs:

A national health service, where medical services are delivered via government-salaried physicians, in hospitals and clinics that are publicly owned and operated—financed by the government through tax payments. There are some private doctors but they have specific regulations on their medical practice and collect their fees from the government. The U.K., Spain, and New Zealand employ such a system. [65]

A national health insurance system, or single-payer system, in which a single government entity acts as the administrator to collect all health care fees, and pay out all health care costs. Medical services are publicly financed but not publicly provided. Canada, Denmark, Taiwan, and Sweden have single-payer systems.

A multi-payer health insurance system, or all-payer system, which provides universal health insurance via “sickness funds,” used to pay physicians and hospitals at uniform rates, thus eliminating the administrative costs for billing. This method is used in Germany, Japan, and France.[66]

A universal mandate for health care coverage defines these systems. Such a mandate eliminates the issue of paying the higher costs of the uninsured, especially for emergency services due to lack of preventative care.[67] Other methods for reducing costs may include:

Funding health care costs in relation to income rather than risk or people’s medical history.[68]

Negotiating the price of prescription drugs and bulk purchasing of prescription medications and durable medical equipment is a method used in other countries for lowering costs. This has been effectively used by the U.S. Department of Veterans Affairs, Medicaid, and Health Management Organizations in the U.S. Yet, it has been prohibited by law from traditional Medicare. Savings of up to five percent of total health care expenditures could result from the full adoption of these practices.[69]

An International Case Study: How Germany Pays for Health Care

Germany has one of the most successful health care systems in the world in terms of quality and cost. Some 240 insurance providers collectively make up its public option. Together, these non-profit “sickness funds” cover 90 percent of Germans, with the majority of the remaining 10 percent, generally higher income Germans, opting to pay for private health insurance. The average per-capita health care costs for this system are less than half of the cost in the U.S. The details of the system are instructive, as Germany does not rely on a centralized, Medicare-like health insurance plan, but rather relies on private, non-profit, or for-profit insurers that are tightly regulated to work toward socially desired ends—an option that might have more traction in the U.S. political environment.[70]

The average insurance contributions to German sickness funds are based on an employee’s gross income, around 15.5 percent with an income cap at $62,781, and employers and employees each pay about half of the premium. Generally, an individual employee’s contribution is 8.2 percent and the employer pays the remaining 7.3 percent.[71] [72]

Premiums are not based on risk and are not affected by a person’s marital status, family size, or health. Germans have no deductibles and low co-pays.[73]

Doctors are private entrepreneurs and get a fee from insurers for every visit and procedure they perform. However, they are tightly regulated. Groups of office-based physicians in every region negotiate with insurers to arrive at collective annual budgets. Doctors must remain in these budgets, as they do not receive additional funding if they go over. This helps keep health care costs in check and discourages unnecessarily expensive procedures. The average German doctor also makes about one-third less per year than in the U.S., around $123,000.[74]

Government general revenues cover premiums for children, on the premise that the next generation should be the entire nation’s fiscal responsibility, instead of just the responsibility of the parents.[75]

Germany reformed its coverage for prescription drugs in 2010 after costs for prescription drugs continued to rise. Prior to reforms, drug companies set the price for new drugs and were not required to show that the new drug was an improvement over previously available prescription drugs. Pursuant to the reforms effective in 2011, manufacturers could set the price for the first 12 months a new drug is on the market. “As soon as the drug enters the market, a new process of benefit assessment begins.” Manufacturers must establish, through comparative effective research that the new drug has an “added benefit to the patient, compared to the previously existing standard treatment.” Drugs without added benefit will be reimbursed according to a government pricing list. New drugs without added benefits are available to patients, but the patient has to pay the price difference. For drugs with added benefit, a price will be negotiated between health insurers and the manufacturer.[76]

Quality of U.S. Health Care in an International Context

U.S. health care specialists are among the best in the world. However, treatment in the U.S. is inequitable, overspecialized, and neglects primary and preventative care.[77] The end result of the U.S. approach to health care is poorer health in comparison to other advanced industrialized nations. According to the Commonwealth Fund Commission, in a 2014 comparison with Australia, Canada, France, Germany, the Netherlands, New Zealand, Norway, Sweden, Switzerland, the U.K., the U.S. ranked last overall. In terms of quality of care, the U.S. ranked fifth, but came in last place in efficiency, equity, and healthiness of citizens’ lives.[78]Comparing other health care indicators in an international context underscores the dysfunction of the U.S. health care system.

Despite the relatively high level of health expenditure, in the U.S. there are fewer physicians per capita than in most other OECD countries. In 2013, the U.S. had 2.6 practicing physicians per 1,000 people—below the OECD average of 3.3.[79]

In the U.S., there are only about 1.2 primary care physicians per 1,000 people. Projections indicate that the U.S. will need 52,000 more primary care physicians by 2025 to meet demand.[80] While population growth and aging make up a substantial proportion of this increased need, expanded access to insurance under the Affordable Care Act means more people will seek out treatment. Therefore, there are provisions in the legislation to increase the number of primary care physicians in the U.S.

There is a significant spatial mismatch within the United States for physicians as well. While the U.S. averaged 225.6 doctors active in patient care per 100,000 people in 2014, there is a wide variance across states; Massachusetts ranks highest with 349.5 active doctors per 100,000 people, while Mississippi has only 170.3.[81]

In 2013, the U.S. infant mortality rate was 5.96 per 1,000 live births[82], while the OECD median was 3.8.[83]

The obesity rate among adults in the U.S. was 35.3 percent in 2013, down slightly from 36.5 in 2011. This is the highest rate among OECD countries. The average for the OECD countries was 19.0 percent in 2013.[84]

Related reading:

Interested in learning about the impact unionizing can have on health care benefits?

I'm a Professional. What can a union do for me?

The Union Difference for Working Professionals

Interested in learning more about challenges for health care professionals?

Safe Staffing: Critical for Patients and Nurses.

August 2016

[1] “National Health Expenditures 2014 Highlights” Center for Medicare and Medicaid Services. Available at: https://www.cms.gov/research-statistics-data-and-systems/statistics-trends-and-reports/nationalhealthexpenddata/nationalhealthaccountshistorical.html

[2] Jessica C. Smith and Carla Medalia, U.S. Census Bureau. Current Population Reports, pg 5 Health Insurance Coverage in the United States: 2014, U.S. Government Printing Office, Washington, DC, 2015.

[3] OECD (2015), Health at a Glance 2015: OECD Indicators, OECD Publishing. Available at: http://www.oecd-ilibrary.org/social-issues-migration-health/health-at-a-glance_19991312

[4] OECD (2015), Health at a Glance 2015: OECD Indicators, OECD Publishing. Available at: http://www.oecd-ilibrary.org/social-issues-migration-health/health-at-a-glance_19991312

[5] Ibid.

[6] Ibid.

[7] Chart source: OECD (2015), Health at a Glance 2015: OECD Indicators, OECD Publishing. Available at: http://www.oecd-ilibrary.org/social-issues-migration-health/health-at-a-glance_19991312

[8] Ibid.

[9] Karen Davis, Kristof Stremikis, David Squires, and Cathy Schoen “Mirror, Mirror on the Wall: How the Performance of the U.S. Health Care System Compares Internationally, 2014 Update,” The Commonwealth Fund Commission on a High Performance Health System, June, 2014, 11. Available at: http://www.commonwealthfund.org/~/media/files/publications/fund-report/2014/jun/1755_davis_mirror_mirror_2014.pdf

[10] Ibid.

[11] U.S. Department of Health & Human Services, Health System Measurement Project, “Percentage of People Who Did Not Receive or Delayed Needed Care Due to Cost in the Past 12 Months.” Available at: https://healthmeasures.aspe.hhs.gov/measure/282

[12] Adara Beamesderfer and Usha Ranji. “U.S. Health Care Costs.” Background Brief. Kaiser Family Foundation. February 2012.

[13] OECD (2015), Health at a Glance 2015: OECD Indicators, OECD Publishing. Pg 31. Available at: http://www.oecd-ilibrary.org/social-issues-migration-health/health-at-a-glance_19991312

[14] The Dartmouth Atlas of Health Care. “End of Life Care”. 2013. Available at: http://www.dartmouthatlas.org/keyissues/issue.aspx?con=2944

[15] National Research Council. U.S. Health in International Perspective: Shorter Lives, Poorer Health. Washington, DC: The National Academies Press, 2013.

[16] Adara Beamesderfer and Usha Ranji. “U.S. Health Care Costs.” Background Brief. Kaiser Family Foundation. February 2012.

[17] “Key Features of the Affordable Care Act, By Year.” U.S. Department of Health and Human Services. Washington, D.C. Available at: http://www.hhs.gov/healthcare/about-the-law/preventive-care/index.html

[18] Ezra Kelin. “Administrative Costs in Healthcare: A Primer”. The Washington Post. July 7, 2009. Available at: http://voices.washingtonpost.com/ezra-klein/2009/07/administrative_costs_in_health.html

[19] Ibid.; Elizabeth Winkler, Peter Basch, and David Cutler. “Paper Cuts: Reducing Health Care Administrative Costs”. Center for American Progress. June 2012. Available at: http://www.americanprogress.org/wp-content/uploads/issues/2012/06/pdf/papercuts_final.pdf

[20] “Key Features of the Affordable Care Act, By Year.” U.S. Department of Health and Human Services. Washington, D.C. Available at: http://www.healthcare.gov/law/timeline/full.html

[21] Michelle Long, Matthew Rae, Gary Claxton; Anne Jankiewicz; David Rousseau, “Recent Trends in Employer-Sponsored Health Insurance Premiums” Journal of the American Medical Association. January 5, 2016. Available at: http://jama.jamanetwork.com/article.aspx?articleid=2480470

[22] Ibid.

[23] Peter Harbage, Ben Furnas, “The Cost of Doing Nothing on Health Care,” Center for American Progress, 2009. Available at: http://www.americanprogress.org/issues/2009/05/pdf/cost_doing_nothing.pdf

[24] “Everyone Gets Sick. Not everyone has time to get better: A briefing book on establishing a paid sick leave standard.” National Partnership for Women and Families, July 2011. Available at: http://www.nationalpartnership.org/site/DocServer/PSD_Briefing_Book.pdf

[25] Melissa Majerol, Vann Kewkirk, and Rachel Garfield, “The Uninsured: A Primer – Key Facts About Health Insurance and The Uninsured in the Era of Health Reform”, Kaiser Family Foundation, November 2015. Available at: http://kff.org/uninsured/report/the-uninsured-a-primer-key-facts-about-health-insurance-and-the-uninsured-in-the-era-of-health-reform/

[26] Kaiser Family Foundation, “Key Facts About the Uninsured Population,” 2015.

[27] Kaiser Family Foundation, “Health Insurance Coverage of the Total Population.”2014. Available at: http://kff.org/other/state-indicator/total-population/

[28] Employer Health Benefits 2015 Annual Survey,” Kaiser Family Foundation, 2015. Available at: http://kff.org/report-section/ehbs-2015-section-two-health-benefits-offer-rates/

[29] By Jessica C. Smith and Carla Medalia, U.S. Census Bureau. Current Population Reports, Health Insurance Coverage in the United States: 2014, pg 10 U.S. Government Printing Office, Washington, DC, 2015.

[30] Employer Health Benefits 2015 Annual Survey,” Kaiser Family Foundation, 2015. Available at: http://kff.org/report-section/ehbs-2015-section-two-health-benefits-offer-rates/

[31] Carmen DeNavas, Bernadette D. Proctor, Jessica C. Smith. U.S. Census Bureau. Current Population Reports

Income, Poverty, and Health Insurance Coverage in the United States: 2009 pg 25 U.S. Government Printing Office, Washington, DC, 2010. Available at: https://www.census.gov/library/publications/2010/demo/p60-238.html

[32] By Jessica C. Smith and Carla Medalia, U.S. Census Bureau. Current Population Reports, Health Insurance Coverage in the United States: 2014, pg 7 U.S. Government Printing Office, Washington, DC, 2015.

[33] Ibid.

[34] By Jessica C. Smith and Carla Medalia, U.S. Census Bureau. Current Population Reports, Health Insurance Coverage in the United States: 2014, pg 15 U.S. Government Printing Office, Washington, DC, 2015.

[35] “The Uninsured and the Difference Health Insurance Makes,” Kaiser Family Foundation, September 2010, 1. Available at: http://www.kff.org/uninsured/upload/1420-12.pdf

[36] Kaiser Family Foundation, “Health Insurance Coverage of Children 0-18” State Health Facts. 2014. Available at: http://kff.org/other/state-indicator/children-0-18/

[37] “Policy Priorities: Uninsured Children,” Children’s Defense Fund, 2009. Available at: http://www.childrensdefense.org/policy-priorities/childrens-health/uninsured-children/

[38] “Women and Health Care in the United States.” National Women’s Law Center, May, 2013. Washington, D.C. Available at: http://www.nwlc.org/sites/default/files/pdfs/2012aca-factsheets/us_062012healthstateprofiles.pdf

[39] By Jessica C. Smith and Carla Medalia, U.S. Census Bureau. Current Population Reports, Health Insurance Coverage in the United States: 2014, pg 13. U.S. Government Printing Office, Washington, DC, 2015.

[40] “The Uninsured and The Difference Health Insurance Makes,” Kaiser Family Foundation, September 2012, 1. Available at: http://kff.org/health-reform/fact-sheet/the-uninsured-and-the-difference-health-insurance/

[41] Employer Health Benefits 2015 Annual Survey,” Kaiser Family Foundation, 2015. Available at: http://kff.org/report-section/ehbs-2015-section-two-health-benefits-offer-rates/

[42] Ibid.

[43] Ibid.

[44] U.S. Department of Labor, Bureau of Labor Statistics. Employee Benefits in the United States, Table 2 and Table 6; March 2015. Available at: http://www.bls.gov/news.release/pdf/ebs2.pdf

[45] Jenifer MacGillvary, “Family-Friendly Workplaces: Do Unions Make a Difference?” UC Berkley Labor Center, July 2009. Available at: http://laborcenter.berkeley.edu/jobquality/familyfriendly09.pdf

[46] “Total Medicare Reimbursements per Enrollee”. The Dartmouth Atlas of Health Care. Lebanon, NH. 2013. Available at: http://www.dartmouthatlas.org/data/table.aspx?ind=225&loct=3&tf=34&ch=191

[47] Employer Health Benefits 2015 Annual Survey,” Kaiser Family Foundation, 2015, 26. Available at: http://files.kff.org/attachment/report-2015-employer-health-benefits-survey

[48] Ibid.

[49] Battista M.D., John R. “An International Perspective on Health Care Reform,” Grand Rounds, Department of Medicine, Stamford Hospital, Stamford, CT, October 8, 2008. Available at: http://www.pnhp.org/news/2009/january/an-international-perspective-on-health-care-reform; Sarah Arnquist, “Health Care Abroad: Japan,” New York Times, August 25, 2009. Available at: http://prescriptions.blogs.nytimes.com/2009/08/25/health-care-abroad-japan/

[50] Austin, Daniel A. “Medical Debt as a Cause of Consumer Bankruptcy”, Maine Law Review, Vol 67, No. 1 pp 1-23 (2014). Retrieved from: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2515321

[51] Christina Lamontage, “Nerdwallet Health finds Medical Bankruptcy Accounts for Majority of Personal Bankruptcies” Nerdwallet. June 19, 2013.

[52] Ibid.

[53] Stech, Katy “The Future of Personal Bankrupcty in a Post-Obamacare World” The Wall Street Journal. July 1, 2015. Retrived from: http://blogs.wsj.com/bankruptcy/2015/07/01/the-future-of-personal-bankruptcy-in-a-post-obamacare-world/

[54] Melissa Majerol, Vann Kewkirk, and Rachel Garfield, “The Uninsured: A Primer – Key Facts About Health Insurance and The Uninsured in the Era of Health Reform”, Kaiser Family Foundation, November 2015. Available at: http://kff.org/uninsured/report/the-uninsured-a-primer-key-facts-about-health-insurance-and-the-uninsured-in-the-era-of-health-reform/

[55] Ibid.

[56] “State Health Insurance Exchange: State Run Exchanges”, ObamacareFacts.com. Available at: http://obamacarefacts.com/state-health-insurance-exchange/

[57] Davis Cusano and Kevin Lucia, “Implementing the Affordable Care Act: Promoting Competition in the Individual Marketplaces” The Common Wealth Fund, February 4, 2016. Available at: http://www.commonwealthfund.org/publications/issue-briefs/2016/feb/aca-competition-individual-marketplaces

[58] Ibid.

[59] Melissa Majerol, Vann Kewkirk, and Rachel Garfield, “The Uninsured: A Primer – Key Facts About Health Insurance and The Uninsured in the Era of Health Reform”, Kaiser Family Foundation, November 2015. Available at: http://kff.org/uninsured/report/the-uninsured-a-primer-key-facts-about-health-insurance-and-the-uninsured-in-the-era-of-health-reform/

[60] Ibid.

[61] Ibid.

[62] “The Affordable Care Act: A Brief Summary”, National Conference of State Legislatures, March 2011. Available at: http://www.ncsl.org/research/health/the-affordable-care-act-brief-summary.aspx

[63] “Summary of the Affordable Care Act”, The Kaiser Family Foundation. April 25, 2013. Available at: http://kff.org/health-reform/fact-sheet/summary-of-the-affordable-care-act/

[64] Ibid.

[65] “Health Care Systems—Four Basic Models,” Physicians for a National Health Program, December 2008. Available at: http://www.pnhp.org/single_payer_resources/health_care_systems_four_basic_models.php

[66] Ibid.

[67] Battista, “An International Perspective on Health Care Reform.”

[68] Ibid.

[69] Ibid.

[70] Richard Knox, “Most Patients Happy With German Health Care,” NPR, August 5, 2009. Available at: http://www.npr.org/templates/story/story.php?storyId=91971406; Uwe Rienhart, “Health Reform Without a Public Plan: The German Model,” New York Times, April 17, 2009. http://economix.blogs.nytimes.com/2009/04/17/health-reform-without-a-public-plan-the-german-model/.

[71] Frequently Asked Questions About Health Care Coverage In Germany,” American Voices Abroad Berlin, 2009. Available at: http://americanviewsabroad.org/FAQs_about_healthcare_in_Germany_v4.pdf

[72] Elias Mossialos, Martin Wenzl, Robin Osborn and Chloe Anderson “ International Profiles of Healthcare Systems, 2014” The Commonwealth Fund. January 2015. Available at: http://www.commonwealthfund.org/~/media/files/publications/fundreport/2015/jan/1802_mossialos_intl_profiles_2014_v7.pdf?la=en

[73] Ibid.

[74] Richard Knox, “Most Patients Happy With German Health Care.” Richard Knox, “Keeping German Doctors On A Budget Lowers Costs,” NPR, July 2, 2008. Available at: http://www.npr.org/templates/story/story.php?storyId=91931036

[75] Uwe Rienhart, “Health Reform Without a Public Plan: The German Model.”

[76] Daniel Bahr and Thomas Huelskoetter, “Comparing the Effectiveness of Prescription Drugs: The German Experience,” Center for American Progress, May 21, 2014.

[77] James S. Cox, “The Future of Health Care,” MD News, August 29, 2011.Available at: http://www.mdnews.com/news/2011_08/05708_foh2011_the-future-of-health-care

[78] Davis,et. al. “Mirror, Mirror on the Wall: How the Performance of the U.S. Health Care System Compares Internationally, V.

[79] OECD (2015), Health at a Glance 2015: OECD Indicators, OECD Publishing. Available at: http://www.oecd-ilibrary.org/social-issues-migration-health/health-at-a-glance_19991312

[80] Petterson S et al. “Projecting US Primary Care Physician Workforce Needs: 2010-2025.”

Annals of Family Medicine, Vol. 10, No. 6, 503-509; 2012.

[81] “2015 State Physician Workforce Data Book” Association of American Medical Colleges, Washington, D.C. 2015. Available at: https://www.aamc.org/data/workforce/reports/442830/statedataandreports.html

[82] “Deaths: Final Data for 2013”, The Centers for Disease Control and Prevention, National Vital Statistics Reports. Vol 64, No. 2. February 16, 2016. Available at: http://www.cdc.gov/nchs/fastats/infant-health.htm

[83] OECD (2015), Health at a Glance 2015: OECD Indicators, OECD Publishing. Available at: http://www.oecd-ilibrary.org/social-issues-migration-health/health-at-a-glance_19991312

[84] Ibid.